EXECUTIVE SUMMARY

The West Coast remains a geographically isolated energy island. While national fuel prices fluctuate based on crude, the West Coast is uniquely burdened by a "Regulatory Wall" of state taxes and a "Conflict Premium" resulting from the 2026 blockade of the Strait of Hormuz.

> I. Regional Fuel Scenarios

Washington & Oregon

- WA Consumption: ~9.6M Barrels/Month. Sources: 45% Canada (Pipeline), 40% Alaska (Tanker).

- OR Dependence: Zero refineries. 85% of fuel arrives via the Olympic Pipeline from WA.

California

Relies on foreign imports for 61% of crude due to a 70% decline in in-state production.

> II. Historical Pipeline Thwarting

The Kinder Morgan "Freedom Pipeline" (Texas to CA) was scrapped in 2013 due to a regulatory wall. This forced West Coast refiners to bypass stable domestic crude in favor of volatile global imports.

> III. Transport Cost Matrix

| Method | Cost / Barrel | Retail Impact |

|---|---|---|

| Pipeline | $5.00 | Most Stable |

| Tanker (Foreign) | $8.00 - $12.00 | Subject to War Risk |

| Rail (Bakken) | $12.00 - $15.00 | Adds ~20¢/Gallon |

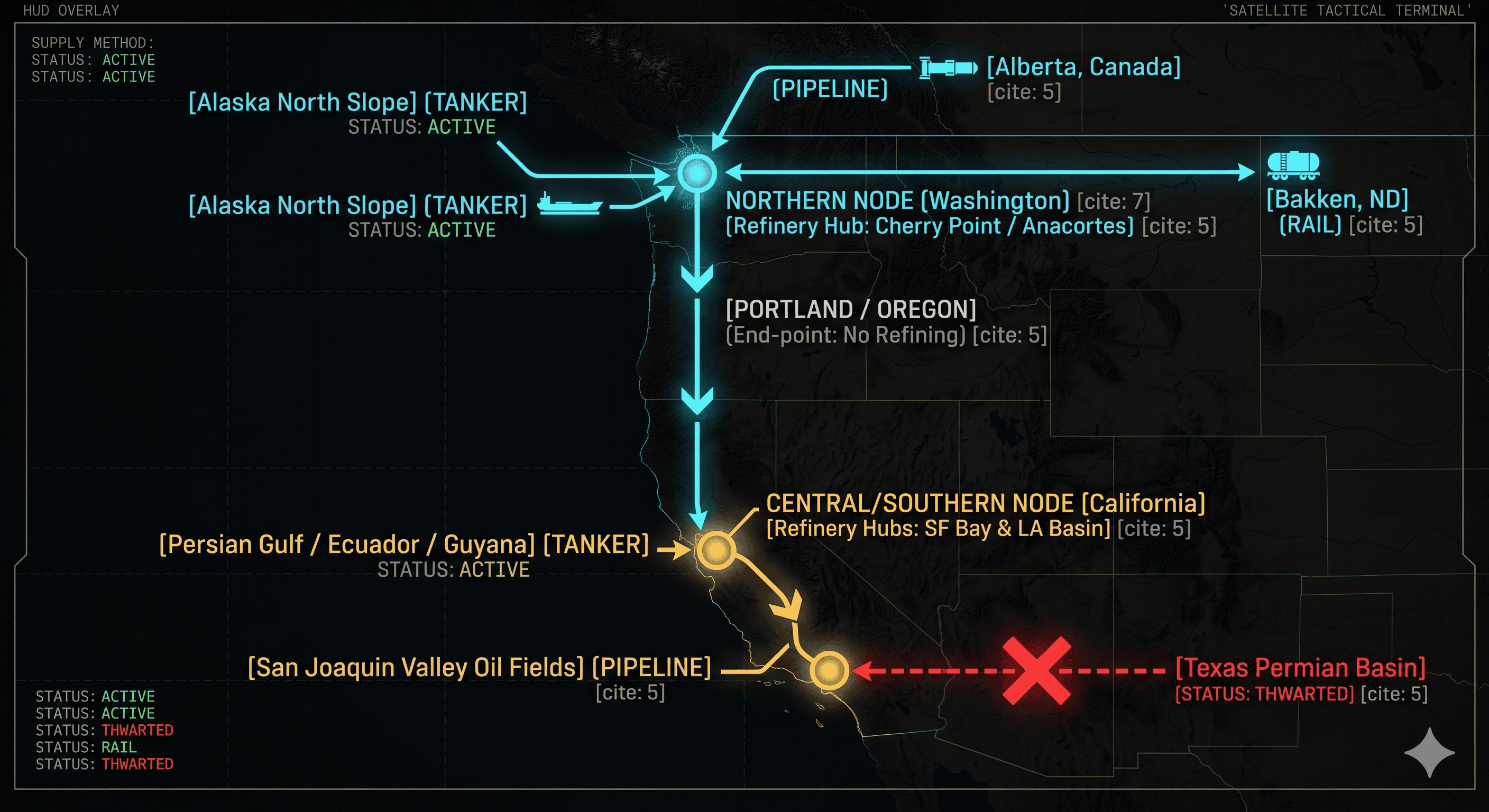

> IV. Conceptual Node Map

NORTHERN NODE (Washington)

[ Refinery Hub: Cherry Point / Anacortes ]

|

|<--- (PIPELINE) --- [ Alberta, Canada ]

|<--- (TANKER) --- [ Alaska North Slope ]

|<--- (RAIL) --- [ Bakken, ND ]

|

V

[ PORTLAND / OREGON ] (End-point: No Refining)

|

|

CENTRAL/SOUTHERN NODE (California)

[ Refinery Hubs: SF Bay & LA Basin ]

|

|<--- (TANKER) --- [ Persian Gulf / Ecuador / Guyana ]

|<--- (PIPELINE) --- [ San Joaquin Valley Oil Fields ]

|

X --- (BLOCKED) --- [ Texas Permian Basin ]

> V. State Fuel Pump Taxation (2026)

Taxes at the pump on the West Coast are indexed to inflation and further layered with climate-related carbon fees.

| State | Excise Tax | Carbon/Climate Fees | Total Tax (Inc. Fed 18.4¢) |

|---|---|---|---|

| California | 70.9¢ | 42.0¢ | $1.31 / Gallon |

| Washington | 59.0¢ | 52.0¢ | $1.29 / Gallon |

| Oregon | 40.0¢ | 13.0¢ | 71.4¢ / Gallon |

Price Components: $5.00 Gallon

Crude Oil (50%)

Refining Costs (15%)

Distro & Marketing (10%)

Combined Taxes (25%)

War vs. Climate: Cost Per Gallon Impact

Hormuz Blockade / "Trump War" Premium ($1.16/gal)

Climate Carbon Fees (42¢-52¢/gal)

Other Fuel Costs (Crude/Excise/Distro)